Global Resources Investment Trust (GRIT). Mispriced opportunity – price target 20p

By Richard Jennings, CFA

Global Resources Investment Trust (GRIT) was set up by RDP Fund Management (run by David “Sam” Hutchins & Kjeld Thygesen) in March of 2014.

The structure of this trust is not like the typical closed end fund, where a monetary subscription is made by investors and the funds are then invested in a diverse portfolio of companies. It is in fact a rather more innovative one, in which constituents swap stakes in their companies for paper in GRIT.

The mechanics of this type of company were borne of the bear market in precious metals and resources stocks as a way for many of these smaller resource companies in particular, to raise cash in an alternate manner given the then ceasing up of capital markets (both debt and equity) in that sector. Of course, the success of such a venture relied upon two things – first and foremost the quality of the constituent portfolio companies swapping their equity for the GRIT paper (which is the basket vehicle for the full portfolio) and secondly, secondary market demand for the paper of GRIT as the companies swapping their equity would at some point patently require to sell their GRIT holding for cash to further their own operations.

Sadly, for all the constituent companies and the immediate secondary market buyers, the bear market in precious metals set in in 2012 – to the defence of RDP, many other industry experts and analysts saw value in 2014, including me. But the depth of the most recent bear market proved to be record breaking, as the chart of the Arca Gold Bugs Index below illustrates all too clearly.

Arca Gold Bugs Index weekly chart

To cut a long story short, and save picking over the unfortunate timing of the launch of the GRIT vehicle, as the bear market intensified for resource stocks during 2014 and 2015, the after-market demand was simply not there and the trust fell to a wide discount, initially of circa 10-20%, to NAV. Many of the portfolio companies simply had no choice but to sell their holdings in GRIT, at whatever price they could achieve, in order to raise cash for their operations. It is worth reflecting on the fact that the original value of the portfolio was circa £40 million.

What increased the crescendo to the downside for the stock price during the latter stages of 2015 was the fact that at launch of the vehicle, the fund managers decided to “gear” the trust. That is the company issued Convertible Unsecured Loan Notes (CULS) of, at the time, some £4.85 million to a few investors – the anchor one being LIM Asia Multi-Strategy fund which currently holds £3.5 million of these notes (the aggregate outstanding was later topped up to a gross £5m of the loan notes. The CULS carry a coupon of 9% and as the portfolio has fallen in value the effects of gearing on the downside have made themselves felt very acutely to GRIT shareholders.

The catalyst for the, quite frankly, ridiculous entertainment of the recent “take under” approach by Primestar of the UAE in late January was the fact that the CULS required, aside from a cash buffer of just under £500,000 within GRIT, that the portfolio of companies maintained a minimum cover of 4.1 times the outstanding principal on the notes. The portfolio fell through this covenant level in October of last year. At that point the fund managers who were holding some of the loan notes decided to convert their holding into stock at a price of 75p. Note that this compared to a then stock price of around 8p per share. That is correct – near 10 times the then stock price.

This was done as a last ditch measure by RDP to try and avoid the repercussions of the breach and I believe they deserve credit for that at least. There was also an intermediate relaxation of the covenants’ NAV cover to 3.6 times and then further relaxed to 3.4 times, but this was removed at the end of February.

Primestar debacle

As the company was in breach of the loan covenant, the CULS holders, of which LIM are the primary holder, were able to force the company into a run-off and, scenting blood in the water, Primestar effectively offered to inject capital into the company at an over 90% pre-dilution discount to the fund’s NAV. This structure was nothing more than a stitch up of existing shareholders in order to fund the redemption of LIM and I made this point clear to the Board and the fund managers in no uncertain terms. Following dialogue between the Board and myself, and an all-round dissatisfaction with the conduct of Primestar during the faux due diligence stage, thankfully for existing GRIT shareholders these UAE chancers were sent packing, to the credit of Chairman Lord St John of Bletso.

So, where do existing and new potential shareholders stand now? We believe that the market has got this one quite simply dramatically wrong. As ever, in part because of an almost complete absence of research. Enter Align…

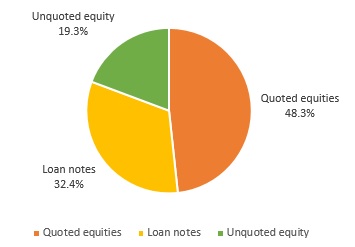

Below is a breakdown of the current portfolio, splitting it into quoted equities (and thus relatively liquefiable), unquoted equities, and some specific loan notes.

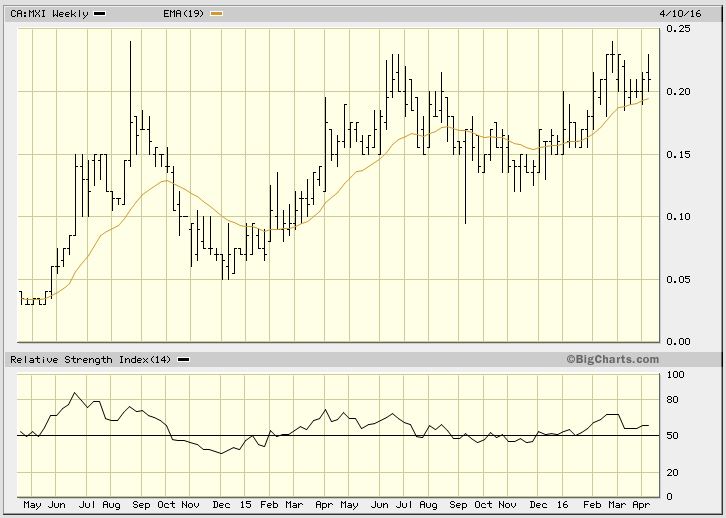

The largest holding within the quoted portfolio is Canada listed Merrex Gold. The company has had quite a rally this last year on speculation of a full takeover by IAMGold following the increasing of IAG’s stake in Merrex in November 2015 to 25.2% (see here – http://www.merrexgold.com/s/NewsReleases.asp?ReportID=729697&_Title=IAMGOLD-Increases-Ownership-to-25).

GRIT holds 29m shares in Merrex and at the current price (15th April 2016) of 21c and based upon an FX rate of 1.82 CAD to the Pound, coincidentally the value of this holding is c.£3.34 million – near as damn it the value of the LIM CULS holding of £3.5 million of which they want redemption.

Merrex Gold chart

Should the Merrex stake be sold by GRIT around the current stock price, the necessity for an orderly run off of the portfolio (and which we believe would likely result in multiples of the current stock price being returned to shareholders in any event) is gone and the pressure from LIM no more.

The opportunity

It is worth pointing out at this stage that the last published NAV (12th April 2016) for the company was just under 32p. This NAV (net asset value) is of course after accounting for the redemption of the CULS at par too. In the event that LIM are repaid then the NAV becomes much more solidified and the covenant breach is gone, as well as a drag of over £300,000 on the company’s NAV in interest payments.

What the market is effectively saying at the current stock price, is that balance of the company’s portfolio, as represented in the pie chart above, is likely to realise just over 15% of the current market value. We just done see it as we will show below.

To illustrate this point, from the most recent portfolio breakdown we have the next biggest holding in the quoted element as Nulegacy Gold (also Canadian listed). We highlight this announcement here – http://www.marketwired.com/press-release/nulegacy-gold-closes-667-million-strategic-investment-by-oceanagold-corporation-tsx-venture-nug-2114688.htm. We also believe that this is a potential precursor to an outright takeover – GRIT holds 20 million shares. At the most recent stock price of 21c this equates to c.£2.3 million at current FX rates. The net effect of this is that we believe there is a potential ready buyer for Nulegacy, as in the case of Merrex with IamGold. OceanaGold is a $1.87 billion mining giant which clearly sees value in NuLegacy and GRIT are holding a key strategic stake of just under 10%. That is a good position to be in.

With £1.25 million of CULS outstanding post any redemption of LIM and just under 40 million shares in existence, at a current share price of 5p (most recent) and so an enterprise value of £3.25 million, the Nulegacy gold position alone accounts for c.70% of the EV. We have been ultra conservative in our valuing of the balance of the quoted portfolio of stocks in the UK, Australia and Canada in writing down to zero a couple of suspended stocks going through reorganisations (Sniper Resources & Portex Minerals) even though we expect there to be residual value in these. We have also written to zero the holding in IMC Exploration listed on the ISDX given the illiquidity of this market but note that RDP still value this at £240,000.

Let’s take a moment with the maths

The aggregate quoted portfolio (including a relatively small holding in Waterberg Coal in Australia that is suspended pending a recapitalisation) is thus valued at c.£9 million. There are £4.75 million of CULS outstanding, leaving a residual value of £4.25 million. We also understand the company is holding a cash buffer of just under £500,000 and so we have approx. £4.75 million of relatively liquid value. This equals 12p pence per share.

Now this is where it gets really interesting – the balance of the portfolio, adjusted for assets written down, comprises convertible loan notes in 3 companies – Anglo African Minerals (AAM), Siberian Goldfieds and Arakan Resources and also equity in AAM. Following a recent accounting test for fair value of these loan notes by the fund managers and their advisers, these holdings were valued at approximately £8.2 million. The 2 former companies make up the bulk of this value at c.£6.2 million and brief overview details on each of them are as follows:

![]()

Anglo African Minerals (http://www.angloafricanmineralsplc.com/) – the company was most recently listed on the now defunct GXG exchange. Following the exchange’s closure last August there is currently no quote on AAM equity. However, the company has a very valuable licence in Guinea, with up to 3 billion tonnes of Bauxite. This presentation here is well worth a read to obtain an idea of what underpins the company value – http://www.angloafricanmineralsplc.com/the-company/company-presentation/.

What is important to GRIT shareholders is that AAM appears to be very much a live company with good prospects. Usefully, aside from the equity, GRIT owns a convertible loan note due at the end of this year with accrued back interest that has not been included in the portfolio value. It is my guess that the company will re-list at some point in the near future and that the loan notes give GRIT some good room for negotiation in the event of any equity recapitalisation. The current note conversion price is 8p but with a last traded price of 1.5p the conversion element of the note presently has no worth. The fund managers RDP have the equity value in the books (some 48.15 million shares) at just 0.005p. With GRIT’s stake of just under 24% and written down to £2.4 million we believe that, in unison with the convertible loan notes, there is in fact material upside to the equity holding in AAM on a relist.

Siberian Goldfields is also an interesting company that is presently private but is, as the name suggests, developing gold projects in Russia, specifically in eastern Siberia. Projections put out by management are for the operations to produce 1Mtpa (67% Fe) iron ore, 100,000oz pa gold and 3Mtbpa bismuth. GRIT holds just under £3 million of principal value of convertible loan notes here carrying 15% coupons. Again, an interest deferment is in place and in fact there is almost 2 years of back interest due. We are informed that this interest element is not included in the company’s most recent NAV either. The loan notes here are very beneficial to GRIT as they are (a) a prior and fixed claim above equity holders in Siberian Goldfields and (b) given the interest accrual point, again give the company meaningful “jostle” room in finance rounds and/or a listing. Should the back interest be paid this is another circa £900,000 of potential upside to GRIT shareholders.

The loan notes in Siberian also have another potentially positive twist and that is that they convert into equity upon a listing of the Co at a 25% discount to the IPO price. No firm details are available with regards to a listing date but clearly, given GRIT’s position in Siberian’s capital structure, on any listing, and bearing in mind the resource value of the company’s assets, there could be material upside to the loan notes’ principal value of £3 million.

To conclude on the unquoted element then, Siberian Goldfields and Anglo African Minerals are clearly potentially very valuable holdings and the loan note positioning in the capital profiles of the two companies gives GRIT shareholders much more security over the equity holders. Even applying a 50% haircut to these loan notes, writing off the interest accrual and writing down the Anglo African Minerals equity holding to zero – in other words an armageddon scenario, this still results in equity value to GRIT of just under £3 million – another 7.5p per share.

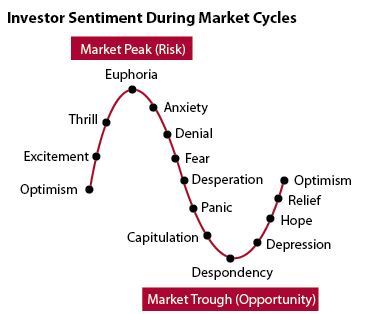

Early stage of recovery swing in Investor Sentiment cycle

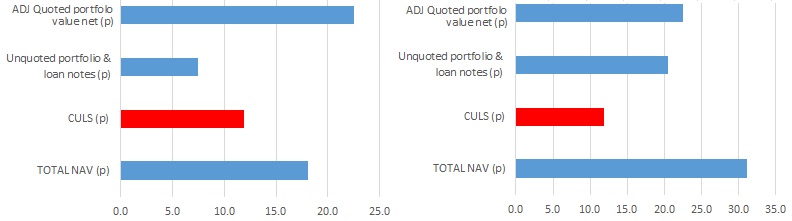

We can see that under pretty much all scenarios including a staged liquidation of the portfolio (something we understand that is being considered), that the equity in GRIT looks to be worth a minimum of c.20p per share. In the event of the main holdings in Anglo African and Siberian listing on the public markets and the loan notes in Arakan, Siberian & AAM being repaid at par then we would be looking at multiples of the current stock price being crystallised to the NAV – with or without the back interest accrual. With just under 40 million GRIT shares in existence, a NAV north of 50p could be possible in the medium term in the event of a successful flotation of Siberian Goldfields given the circa £3 million of CLNs held by GRIT in this.

NAV valuation analysis: Left chart – “armageddon scenario” = 18.1p. Right chart – base case = 31.1p.

For those with an appetite for risk, we see the stock price as an ideal way to position for a continuation of the recent more positive sentiment in the investor sentiment cycle for commodities, where it looks to us as if we are just coming through the “depression” stage below. We believe this cycle has much further to run.

CLEAR DISCLOSURE – A director of Align Research Ltd holds a personal interest in GRIT & is bound to Align Research’s company dealing policy ensuring open and adequate disclosure. Full details can be found on our website HERE