Obtala – Completion of WoodBois acquisition highlights further value potential

By Richard Gill, CFA

Africa focussed forestry and agriculture company Obtala has announced three pieces of news to the market since last Friday afternoon.

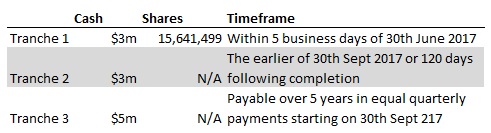

Most importantly, the company has finalised the previously announced acquisition of Gabon timber business Woodbois International through 75% owned forestry subsidiary Argento. The deal, which was completed by 30th June as expected, is for a total consideration of $14.6 million (£11.2 million), payable in a mix of cash and shares over three tranches – see table.

Paul Dolan (CEO) and Warren Deats (COO) have now been appointed to the WoodBois board with WoodBois’ founder directors, Zahid Abbas and Jacob Hansen, remaining with Obtala for a minimum of 5 years. Hadi Ghossein, a Gabonese citizen who manages operations in Gabon, has committed for a minimum of 3 years and will become CEO of new holding company WoodBois Gabon.

As we commented in our note of 24th May, Copenhagen headquartered WoodBois is engaged in the global trading of sawn timber which it sources from 100s of exclusive timber producers throughout Africa, as well as the production of sawn timber planks and veneer from its concessions in Gabon. WoodBois’ concessions in Gabon now total 96,851 hectares (up from 41,278 at the time of the initial acquisition announcement on 24th May following a consolidation of additional permits) and are all located within 70km of the 42,000m³ capacity sawmill and 18,000m³ veneer facility in Mouila, Gabon.

The company is currently planning expansion into Asia, with joint-venture discussions underway with strategic partners in Pakistan, where WoodBois has already secured a contract to provide railway sleepers for the construction of a major railway linking China to Pakistan’s port of Gwadar. For 2016 WoodBois recorded US dollar equivalent revenues of $13.8 million and net profits of $295,000.

The main point which we take from the acquisition completion announcement is that the due diligence exercise substantially verified all assumptions upon which Obtala’s valuation of the business was based and found that many assumptions had been very conservative.

Other key points of the deal include

– Since 24th May WoodBois has received approval for a forest management plan for a 20-year concession covering a net area of 96,851 hectares near Mouila, 82,703 hectares of which is dense forest. Each year WoodBois may apply to harvest an area of 5,000 hectares, and each 5,000 hectare area may remain open for harvesting for up to three years.

– Over 25 commercial species were identified in the forest. An annual potential first and second grade cut of 8,201,091m³ of Okoume, 527,691m³ of Okan, 153,662m³ of Azobe, 926,940m³and 186,925m³ of Ovengkol was found. This assumes approximately 3,000 hectares of each 5,000 hectare area is readily accessible productive land, a conservative assumption.

– WoodBois’ current harvesting capacity was assessed by Obtala’s commercial due diligence team and an independent forestry consultant, concluding an annual harvest of 71,280m³ can be readily achieved with existing equipment. However, given the extent of the timber resources available in the concession there is scope to invest in increasing harvesting capacity many times over. The actual amount harvested however is likely to be drastically less than the company’s allowance due to its commitment to sustainable harvesting practices.

– At the WoodBois’ sawmill, the volume weighted average recovery rate across all species (January-May) was found to be 57.5%, with a target recovery rate of 56% measured by a forestry consultant. Year to date average production cost per m³ sawn timber was found to be $249 per m³, in line with WoodBois estimate of $260, with the operation expected to achieve lower production costs as volumes increase. The annual capacity of the sawmill is estimated at 42,000m³ (vs. 24,000m³) once new equipment (already purchased by WoodBois) is installed.

– Obtala intends to invest $400,000 to compete the construction of WoodBois’ veneer factory in Mouila to achieve an annual production target of 18,000m³ of veneer, expected to be complete by the end of 2017. The veneer business is expected to “contribute significant cashflow from 2018”.

– Obtala intends to significantly upscale the WoodBois trading business, which has seen its available capital reduced as it invested in production assets in Gabon. Obtala has already increased WoodBois credit facility, enabling the business to procure a greater volume of wood from African suppliers (and at higher margin via ‘pre-financing’ production) in 2H 2017. We note Chairman Miles Pelham’s comment that, “…working capital has been the only thing holding back substantial growth in WoodBois’ trading division and we intend to unlock this potential immediately.”

2016 results released and funds received from directors under recent preference share issue

Obtala has also recently announced results for the year to 31st December 2016, although given the recent strategy changes and fundraisings the historic figures are largely immaterial to our investment case. For the record, revenues came in at $0.63 million, with a net loss of $5.6 million.

In addition, the company has confirmed that it has received a total of $2.15 million from four directors who subscribed to the recent preference share issue in subsidiary Argento. Elsewhere, with immediate effect Frank Scolaro will be retiring from the board as Non-Executive Director and Philippe Cohen will be retiring as Finance Director. The board will be looking for a replacement CFO immediately, with interim duties being carried out by Paul Dolan and recently hired Group Accountant Carnel Geddes, who is said to have sufficient capabilities for the task.

Current share price provides attractive entry point

Despite the potential value which both we at Align and Obtala believe that the WoodBois acquisition can deliver over the coming years, the markets have seemingly not reacted. As mentioned in our previous note, having analysed the base financial case for the deal, and applying a similar DCF approach to our core valuation, we believe that WoodBois could add further value to Obtala shareholders of around 13.4p per share – this may prove to be conservative given that the due diligence process highlighted further potential upside. This adds to our DCF valuation of the existing forestry and agriculture assets of 30.52p per share. So with a combined valuation of 43.92p, we see significant potential upside compared to the current market price of 17.375p.

As ever, the main risk for Obtala is execution risk, with a number of tasks still to be completed at its operations before meaningful levels of revenues and profits are being achieved. We retain our stance of Conviction Buy.

DISCLAIMER & RISK WARNING

Obtala is a research client of Align Research. Align Research holds an interest in the shares of Obtala.

This is a marketing communication and cannot be considered independent research. Nothing in this report should be construed as advice, an offer, or the solicitation of an offer to buy or sell securities by us. As we have no knowledge of your individual situation and circumstances the investment(s) covered may not be suitable for you. You should not make any investment decision without consulting a fully qualified financial advisor.

Your capital is at risk by investing in securities and the income from them may fluctuate. Past performance is not necessarily a guide to future performance and forecasts are not a reliable indicator of future results. The marketability of some of the companies we cover is limited and you may have difficulty buying or selling in volume. Additionally, given the smaller capitalisation bias of our coverage, the companies we cover should be considered as high risk.

This financial promotion has been approved by Align Research Limited.