Align Research’s Top 10 Conviction Picks for 2018

Well, it’s that time of year again where we look ahead to the new calendar year and place our “cooking” and conviction picks at Align on show for 2018. Last year’s picks are HERE and we are pleased to relay we had some real winners. ZIOC was the stand out performer – rising from 6.5p to 25p at the peak when we advocated a sell. GRIT also rose to 14.5p at the peak and the only real loser in terms of no tradable profits being presented to be banked was Gulf Keystone in. Even Providence Resources traded up to 18p ahead of the disappointing drill in the South Porcupine that decimated shareholders. We banked good gains on almost all the positions and hope our followers did too.

Without a doubt our most prescient calls in recent months have been Mayan Energy (more on that below), flagging up the blockchain opportunity with Milestone Grp (MSG) and the US generic pharma plays where we called the absolute bottom per HERE and HERE. Are there any lessons that can be learnt from this year including some of our failures of which Arian Silver is the stand out? Yes is the answer. For a start, going forward we will be very, very hesitant in taking on a company with Beaufort Securities as the broker. There is a much wider market issue here with regards to the placings that continuously take place on AIM and where existing minorities seem to run the risk of having their metaphorical “legs cut from beneath them” when the cash run rate is less than 12 months. Prime example being the most recent placing in ValiRx for which we believe there was absolutely no reason.

The other lesson we have learnt is to be very wary of stock where management have nominal “skin in the game” – this was our second error with Arian Silver. This point mixed with Beaufort as the broker means that management are most likely to be frankly indifferent to equity price decimation by way of placings. We cannot stress enough the importance of these points and we certainly will pay very serious heed of these before getting behind a company going forward.

So, without further ado, our Top 10 Conviction Buy calls for 2018 are as follows:

- Mayan Energy – 0.54p

This company has been covered in full HERE and such is our conviction in this that we are one of the largest shareholders in the stock. Remembering our point above re management “skin in the game” we point out that “Eddie” Gonzalez and key partner shareholder David Kahn hold just under 15% between them. They have a serious vested interest to see this minnow re-rate to a more realistic level. Based upon the company’s own financial and production models the next 12 months will certainly not be short if high impact news as more wells steadily come on stream.

Most recently, we note the RNS of 22 December and which the market took negatively. Whilst progress in bringing the wells on stream has been a little slower than expected the eventual prize remains the same and the progress has not been by virtue of poor well stimulation for example but simply permitting delays which is understandable given the time of year we are now at.

There is all to play for here and at the current price of 0.55p new entrants are offered the opportunity to get into the stock at a circa 10% discount to the recent oversubscribed placing. In recent discussions with management we are highly optimistic as to what 2018 will bring, particularly concerning the recent acquisition of Asphalt Ridge.

This recent update HERE sums up succinctly our view on the stock and we believe the shares will deliver a multi-bag return to holders during 2018. Indeed, should the market mark the stock lower in the near term we plan to increase our holding meaningfully as by any measure – current balance sheet situation, pro forma cash flows, Asphalt Ridge value and the targeted 1000bopd by end 18/early 19 the stock is woefully undervalued.

- Gulf Keystone Petroleum – 97p

We did have GKP in as one of our top picks for 2017 and this was effectively the only real disappointer amongst the group in that there was no real trading opportunity to turn a profit. However, over the last 12 months, at an operational level, the company has quietly cracked on with the plans and progress as detailed in their refinancing prospectus of late 2016 whilst the stock price has declined modestly.

News out of Genel Energy in August which detailed an enhanced and evolved payment structure with the Kurdistan Regional Govt (KRG) and a sharp re-rating thereof in that stock led many analysts (including ourselves) to believe that one would follow shortly thereafter for GKP. That such an agreement has not yet been announced coupled with the referendum on independence that was brought by the Kurdish Government in the autumn and that backfired spectacularly on them have served to drag the stock price lower. All the while the price of oil has continued to rise thus making any valuation metric that is based upon reserves relative to Enterprise Value/market cap etc even more compelling.

We see the disconnect between the stock price and its peers as unwarranted and that the market is completely ignoring the fundamental transformation of the company over the last 18 months that will allow them to ramp up production materially at their key Shaikan field. As a consequence of the latent value that we currently see, GKP is now one of our largest positions. Barring a material decline in the price of oil we would not bet against a takeover approach by any number of operators in the region for the company such is the cash flow yield that is on offer and the relative EV/2P discount measure to Genel and DNO in particular.

Starkly, the numbers breakdown as follows to us based on management releases – we believe the cash balance to be around $165m and gross debt at the $100m level. With a current market cap of £223m this results in an Enterprise Value of circa £175m. The shares thus trade at less than 50p per boe before we even begin to factor in residual value for the Shaikan field’s 2C reserves. Put simply the stock is outrageously cheap and the more cash flows are generated against the current oil price the more compelling an acquisition target it becomes to its peers. We thus expect the stock to trade closer to £2 than £1 as we move through 2018.

- Pathfinder Minerals – 1.075p

Our next pick is a binary play. If a deal is done with General Veloso then the shares will likely increased five fold overnight (dependent of course upon such deal terms finer details). If there is no deal then the company most likely will become a shell and another opportunity reversed into it. From a risk/reward basis it looks to us that at 1.1p there is perhaps 10 – 20% downside ref a shell value and upwards of 5, 10 times on an immediate reaction basis to a licence resolution deal and very likely much, much more if the large resources of ilmenite, rutile and zircon are ultimately mined. HERE is our indepth commentary as to why we see value and how we see it playing out.

The raising of capital by the company in early December and the recent commentary of a framework deal in place leads us to believe that the odd of news in this regards being released in early 2018 are shortening by the day. In illustrating our conviction in this call we hold just over 3% of the company.

- Gaming Realms – 8.6p

This is a departure from our predominantly mining picks and HERE is the indepth research we produced on Gaming Realms and HERE our most recent commentary. The deal announced in early Dec with regards to the repayment of the $4.5m due to Real Networks lifted a large question mark over the company re its ability to repay this liability and refinanced the balance sheet on much less onerous terms. Additionally the 5 year basis of the new debt facility gives management the runway to build on the recent momentum of positive cash flows and growing EBITDA.

We recommend our readers to look closely at the full note as to how the fundamentals are expected to play out as we go through 2018 but make the further point that we see the deal with Jackpot Joy as a platform for ultimately a full takeover subject to the anticipated operational performance playing out over the next 12-18 months. With a market cap in excess of £600m on Jackpot Joy ‘s (JPJ) part and GMR capped at present at less than £25m, such an acquisition would be a mere morsel to JPJ and, given the higher rating of JPJ’s stock, would be earnings accretive if done in stock. We do in fact suspect that the convertible basis of the debt is to give JPJ an equity foothold on the register for an outright bid subject to seeing how the tie up plays out.

There has been a seller overhanging the stock for some months now and as is usually the case upon the clearance of such a seller, we would expect the stock to re-rate with a first target the recent placing price of 11p, recalling that management participated in this placing with decent sums too and so new entrants on the register are able to enter at a circa 20% discount. We doubt this discount will last much longer.

At 8.5p we believe GMR to be at least 50% undervalued.

- Cradle Arc (formerly Alecto Minerals) – 10p (post consolidation re-list price)

Cradle Arc (formerly Alecto Minerals) has been suspended for several months now. We expect the company to return to the market in the first half of January and will be releasing a full coverage note on the stock at this point.

At the time of suspension the company was refocusing around the acquisition of the Mowana copper mine in Botswana and which has now completed. We see Botswana as one of the most stable and investment worthy regions on the African continent and view Cradle Arc’s COO Mark Jones in high regard. Combined with the fact that the Mowana mine project has had over $155m spent on it and it is actually producing we see the anticipated re-list level as providing copious amounts of upside for new investors.

We will update more thoroughly on this investment opportunity post the re-list and our full coverage note release but flag this imminent return to the market to our followers as one of our top picks for 2018.

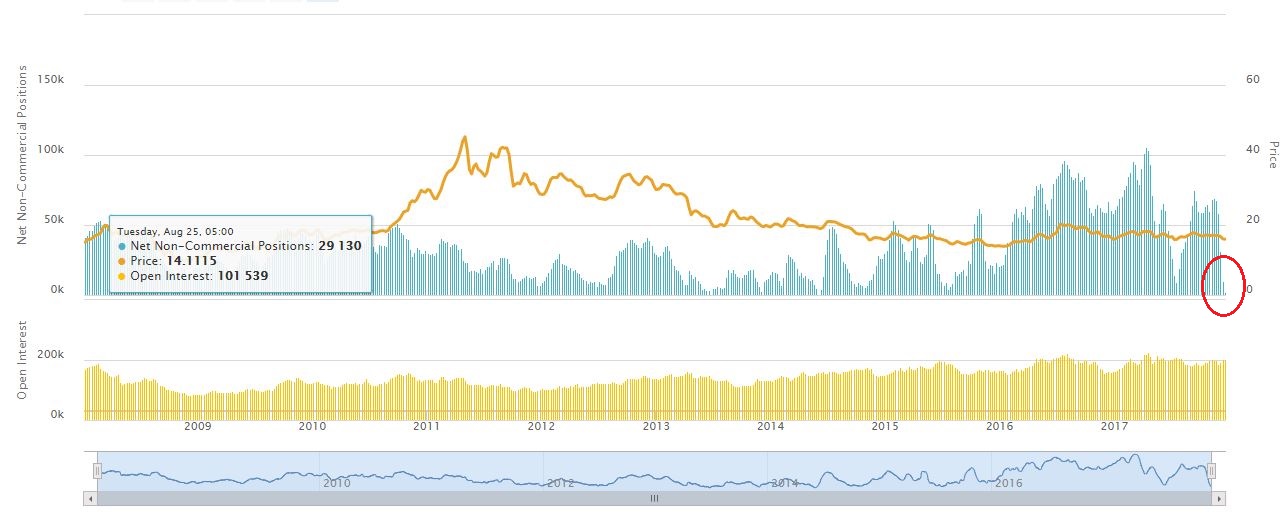

- Silver commodity – $16.34/oz

There have been numerous commentators (including ourselves) that have been bulls of silver for the last 4 years now. Given that the metal has steadfastly refused to break into a bull run it is perhaps not surprising that there are very few this year that we can see that are tipping the commodity as a key call for 2018. Indeed, looking at the COT positioning below we can see that non commercial silver bulls are at the lowest levels for many years (circled in red).

This lack of speculative long positioning and muted bull sentiment when married with the current gold:silver ratio near its historical peaks (which has historically been a reliable precursor to rallies in silver) is music to a contrarian’s ears. We can see in the chart below that the metal has essentially been carving out a basing formation for the last 4 years since the deep sell off from the speculative bubble fervour that took it up to peaks near $50/oz. Indeed, 4 years is generally the extremity of a bear market/basing period after a deep sell off for almost all financial instruments and we can see this by looking at such a period in the Nasdaq in the mid noughties and Japan in the early/mid 90’s.

The current rage is for so called crypto currencies and these seem to have displaced gold and silver as the go to alternate to the equity market. Indeed, the Winklevoss twins have dubbed them as “Gold 2.0”. We are not so sure. What we do know is that the contrarian opportunity that presents itself currently in silver provides for a “cheap” hedge to an equity drawdown and that based upon many other financial and commodity instruments the play set now presented from a positioning and technical perspective provides an attractive long set up. We are long and should there be further weakness in the months ahead will use this to add to our position.

- Acasti Pharmaceuticals – 94c (US)

We have only just released a thorough overview of why we think this stock could deliver tenfold returns, and some, over the next few years. HERE is the full piece.

Potted opportunity set is that set against a current market cap of just under US$23m and pro forma cash (estimated) of circa $20m (including the recently announced Chinese partnership deal and receipt thereof of $8m), should CaPre be successful in Phase III trials as we go through 2018 the stock will likely explode. The marketplace is truly massive given that the product could be prescribed as either an alternate or complementary treatment to statins for high cholesterol given that the market for statins runs to multi billions of dollars . The recent offering and warrant attachment has pulled the stock back from highs over $3 less than a month ago and we have taken this opportunity to add materially to our position.

- Endo Pharmaceuticals – $7.81c (US)

Again, we wrote more fully about this generic pharma play listed in the States HERE and suggest readers condense this fully in understanding the valuation opportunity that we believe is way too low. Since our alerting our followers to this stock in late October the trade has delivered over 30% by way of returns but we believe there is much more to go for. We suspect the late 2017 weakness, in contrast to the other 2 picks in the sector we brought to readers attention per HERE, is due to end of year tax selling and re-iterate our short term price target of $10 given the frankly ridiculous 2018 FCF yield relative to the market cap of near 50%.

- Red Rock Resources – 0.95p

We will shortly release an indepth note on this small cap mining play but at this stage will highlight the primary underpinnings of our enthusiasm – firstly, based upon the anticipated listing price of Jupiter Mines in either Australia or the UK shortly of circa AUD$1bn, RRR’s stake would be worth over 50% more than the current market cap. This leaves the Steelmin project, the gold exposure (and we are very bullish of gold going into 2018), oil and the very interesting cobalt opportunity in the DRC where DD is being carried in for negative value.

Secondly, recent directors buying by Andrew Bell that has materially increased his stake sends a very strong signal to the market as to what the insiders believe of the current market value. At this area of the marketplace it usually pays to follow such buying. No matter how we slice and dice the current SOTP value we arrive at figures that are multiples of the current market cap and accordingly add RRR to our Top 10 for 2018 list.

- Oilex – 0.245p

As with a number of our picks in this list we have covered Oilex recently fully HERE and HERE. The recent news of Republic Investments putting upto £1.33m into the company is solid news for shareholders. The funds will allow drilling to commence at their key Cambay block in India which is a multi trillion cubic feet opportunity. Republic have an enviable track record with their recent investments and together with the catalysts that we see on the horizon during 2018 which include the PSC licence renewal and 9 well workovers it is our contention that none of the newsflow due is remotely reflected in the current stock price and we see value upto 1.6p.

Finally, to conclude, we are expecting the US stock market in particular to finally break this year. Volatility has been subdued for too long, retail investor exposure is nearing levels that historically has forewarned of trouble, sentiment and complacency flash red signals and there are a whole host of geo-political issues that could flare globally, not least war on the Korean peninsula – God forbid if it turns nuclear. Our stance is to remain with the small caps where we can establish that there is solid fundamental backing and near term re-rate catalysts combined with serious asymmetric skew (so muting the impact of systematic risk). We intend to hedge for a larger market routing with long Vix exposure, silver and potentially outright short positions on the US.

Good luck & stay nimble in 2018.

CLEAR DISCLOSURE – The author, who is a Director of Align Research Limited, holds a personal interest in all companies mentioned in this article and is bound to Align Research’s company dealing policy ensuring open and adequate disclosure. Full details can be found on our website here (“Legals”).

This is a marketing communication and cannot be considered independent research. Nothing in this report should be construed as advice, an offer, or the solicitation of an offer to buy or sell securities by us. As we have no knowledge of your individual situation and circumstances the investment(s) covered may not be suitable for you. You should not make any investment decision without consulting a fully qualified financial advisor.

Your capital is at risk by investing in securities and the income from them may fluctuate. Past performance is not necessarily a guide to future performance and forecasts are not a reliable indicator of future results. The marketability of some of the companies we cover is limited and you may have difficulty buying or selling in volume. Additionally, given the smaller capitalisation bias of our coverage, the companies we cover should be considered as high risk.

This financial promotion has been approved by Align Research Limited.