Align Research Top 10 Conviction Picks for 2017

By Richard Jennings, CFA

As another year turns (and we are all, sadly, that bit older!) and we close out our inaugural 12 months here at Align Research we lay out for our readers and subscribers our Top 10 Conviction picks for 2017.

At the start of 2016 we were one of the very few commentators to call the turn of the generational commodities rout that had laid many commodity blue chips low such as Anglo American and Glencore and whom lost multi-billions of market cap during the near 3 year sector routing. Here was our lead in piece to 2016 – http://www.alignresearch.co.uk/gold/the-bull-case-for-commodities-is-stronger-than-ever/ and here is our follow up one we printed 6 weeks later – http://www.alignresearch.co.uk/commodities/standing-in-the-foothills-of-a-commodity-market-bull-run/. Even our bullishness was tempered relative to what was actually delivered however (excerpt – “In my opinion I would not be surprised to see the most beaten down constituents of the 350 Mining Index, increase by 50-100%, with the likes of Anglo American and Glencore being in the vanguard. Their stock prices relative to book value trade for frankly fractions and so if the debt vs equity worries fade the rallies could likely be spectacular”) as many stocks doubled, trebled and more from that point.

As the year progressed we also called the turns in both the oil price and global equity markets too, almost to the tee as we can see HERE and HERE. It’s fair to say we have set ourselves a high target to outperform in 2017 relative to our stance in 2016.

Nevertheless, below are our top 10 picks for 2017 and it goes without saying that such is our conviction in each of these plays that we of course, per Align’s business model, hold positions in each and every one of them.

1. Global Resources Investment Trust – 6.6p.

![]()

Our reasoning is laid out HERE and we are shortly to release an in depth research piece analysing the potential catalysts for a material re-rating that we expect to occur as we progress through 2017. In short, the stock price presently trades at a price that is a discount to its quoted portfolio value plus cash and net of the entire loan repayment. There is zero value being attributed to the company’s positions in both Siberian Goldfields (which is expected to list in 2017) and also Anglo African Mineral (“AAM”) which holds one of the world’s largest bauxite reserves in Equatorial Guinea. This is a very unique situation and one that we are greedily buying into whilst “Mr Market” offers this aberative position. Our buy stance on GRIT is our singularly most high conviction play for 2017 and we expect to achieve multiples of the current stock price as the market cottons onto the mispricing and the material progress AAM in particular has made in progressing this world class bauxite project.

2. Providence Resources – 14.75p

It is no secret that Tony O’Reilly Jnr and I did not swap Xmas cards and greetings this year. HERE is the background as to why I have called for his resignation and been so critical of him. Indeed, I am hard pressed to recall any other company that has wiped shareholders out (at the lows) by near 99% whilst holding next to no personal equity interest in the company and yet the CEO has remained in the seat. Truly one for the business case studies…

That being said, the company does hold material O&G licences off the South and West Ireland coasts and has established 2C resources at Barryroe – the latter which has proved to be so tortuous for shareholders in achieving monetisation. With one of the biggest deep water drills globally lined up for the company’s Druid prospect in the summer of this year and which is targeting over 3bn barrels of oil (with the potential to also drill the Drombeg prospect which is estimated by Schlumberger to hold another 2bn barrels of oil) excitement will build as we get closer to the drill bit turning.

Make no mistake if the Druid well is a success the stock price will be many, many multiples of the current 15p as such is the legacy of failure to commercialise here by ToR Jnr that the shares have effectively zero value for these reserves at present, quite aside from the other portfolio licences including the key Spanish Point and Barryroe prospects. With the 2016 appointment of ex Tullow head honcho Pat Plunkett, we remain hopeful that he really does add some oomph to commercial capabilities in doing deals on the latter to de-risk the company’s profile should Druid not deliver. With institutions holding over 80% of the stock here and the penultimate placing price being 25p back in the spring of 2015, we expect the shares to see little in the way of selling pressure below this point should news flow that was promised for year end 2016 be delivered in the near term.

3. Genel Energy – 75p

![]()

Genel Energy is another of our oil focused plays for 2017; indeed fully 5 out of 10 are in this sector, illustrating to us how, despite a doubling in the oil price from the lows seen in early 2016, many companies valuations are still at multi years in terms of EV/2P basis and offer exceptional value.

Genel’s woes have been well publicised – problems obtaining payment from the KRG, declining production from its Taq Taq field and the perceived lack of progress in progressing its key gas field assets – Bina Bawi and Miran. The market is awaiting an update on these in its operational release slated for 24th January and we expect this update to layout the company’s plans on debt repayment, gas field development and further drilling of their fields. There has been very little fresh information since the announcement in the late spring of 2016 that TEC (a JV incorporating the State owned Turkish Petroleum) were looking to partner with GENL in developing the pipeline to connect the 2 gas fields to Turkey. Any update here could provide a serious catalyst to the upside.

At the current stock price, if we are indeed to ultimately expect repayment of the circa $400m that remains outstanding from the KRG, then the stock now trades (on an EV basis) at less than 1 times pro forma EBITDA. Clearly the market does not believe this will be repaid given the valuation and hence the financial update in 2017 in which management are likely to address this will give us clarity on the likely realisability of this material sum. This could be another catalyst to a material re-rate.

If these emails (https://wikileaks.org/berats-box/emailid/30563) released over the Xmas period by Wikileaks in relation to correspondence between Genel and Hawrami are real (and I have every reason to believe they are), the valuations put out of $2.7bn at a 7.5% discount rate for Bina Bawi and Miran and $414m and $1.2bn for Taq Taq and Tawke respectively illustrate pretty clearly the massive valuation disjoint at play presently in the stock price versus Genel’s underlying assets.

However we dissect the current valuatio, and working on the assumption of a floor price of oil of $45 bbl (less than most commentators), we believe the stock to be dramatically undervalued. With unrisked core NAV around 175p per share, most analysts’ sanguine/negative on the stock (almost always a very good contrary indicator) and the stock now trading at less than $2bbl on an EV/2P basis, we struggle to see any downside here. We see Bina Bawi and Miran as hidden value worth north of 100p per share and the balance E&A portfolio offering upside of upto 200p per share. It is our suspicion that GENL will be the Anglo American of 2017 (the latter increasing near 5 fold in price in 2016).

4. Gulf Keystone Petroleum – 127p

![]()

This is our second Iraqi Kurdistan oil play and we have written about it only recently in relative depth HERE and HERE. We urge readers to read these pieces with regards to the investment case in its restructured form.

Put simply, with DNO having expressed interest in acquiring the company and now China’s SINOPEC we expect a conclusion to this interest in the opening months of 2017. There is in fact market speculation that there is a third (and possibly more) interested party – supposedly from the US and given the lowly valuation of the company’s reserves and the cleaned up balance sheet we will be highly surprised to see these still quoted by the end of 2017. Our expectation is for a final takeout price of circa 180p and we see no downside from here (127p).

5. Zanaga Iron Ore – 6.5p

![]()

See HERE re the background as to the Republic of Congo based world class iron project that ZIOC holds a 50% less 1 share interest in with Glencore. The opportunity holds over 2bn tonnes of iron ore at one of the highest purity levels (66% fe). The trade here is that net of cash the company’s equity trades for a fraction of a fraction of the NPV of the project and we suspect that 2017 will be the year that either a new party is brought into the consortia (likely a Chinese enterprise) to progress development or ZIOC or its partner Glencore look to take ownership of the balance equity in the partnership from the other party. Under any of the scenarios, and using even the written down value of the JV by ZIOC itself (ie a worst case auditors sign off figure) we see a price multiples of the current equity level.

Considering that the iron price has also near doubled from the lows in 2016 and trades around $80/tne together with expectations of both China and the US putting their feet on the growth pedals in 2017, the fundamental backdrop for a re-catalysing of the project are very much intact.

There is a very small free float here too with CEO Clifford Elphick and investor Strata holding in excess of 70% of the company’s equity and so continued positive sentiment could move the shares sharply. Remember the stock originally floated at a value of 156p per share and (rarely for the sector) there has been no additional equity dilution since being quoted. This gives you an idea of what the project was once seen as being worth. At 6.5p entering 2016, we see this as a classic asymmetric risk/reward play as part of a diversified basket of stocks.

6. Zenith Energy – 7p (13c CAD)

We have an update piece coming out shortly on this small cap Azerbaijan operator that is veritably punching above its weight in terms of the SOCAR (State Oil Company of the Republic of Azerbaijan) production sharing JV they entered into in 2016 and that was truly transformational for the company.

Management have just completed a capital raising in London to facilitate a dual listing both here (full list) and in Canada on the TSX-V exchange. The capital raise is to be applied to the work over of their existing Italian assets and to develop further their major fields in Azerbaijan. With a gross all in cash production cost of just $18 b/bl oil at their Azerbaijan fields and an independently verified NPV of their 2P reserves of @ £360m, even though the shares have increased by over 100% from our initiation report HERE we see much more upside during 2017.

Our UK rebased note will be released in the days ahead in which we will elaborate further on the valuation opportunity and expected company progress through 2017.

7. Valeant Pharmaceuticals – $14.5

Many would consider including the embattled US pharma play Valeant which is deemed to be toxic by many within our list of top picks for 2017 crazy, but our positive stance here is borne of 2 elements.In the first instance if one follows the maxim to buy when there is blood on the streets or at the point of maximum despair then going into the closing days of 2016 with the stock down over 94% from its highs and indeed by eight odd percent in 2016 the shares certainly fit

In the first instance if one follows the maxim to buy when there is blood on the streets or at the point of maximum despair then going into the closing days of 2016 with the stock down over 94% from its highs and indeed by eighty odd percent in 2016 the shares certainly fit this bill. Of course, buying a stock that is in the doldrums simply for the sake of it is no strategy and so one must have confidence that the market is overlooking one or more aspects of the business. To me this is simply the prospect of the company filing for bankruptcy in 2017 which the market presently is pricing as a certainty.

Given that the shares trade for around 3 times adjusted earnings then clearly if the expectation of default and/or bankruptcy dissipates the potential for a re-rating is material. One only has to witness the near 40% rally in just a few hours in early November on news of the potential sale of Salix to illustrate very succinctly how the stock is primed for any positive catalysts. Looking at the company’s free cash flow profile during 2016 then I do not see the company (nor does the bonds which is a big “tell”) filing for bankruptcy in the short term. IF they can divest some of their assets and which management have made noises about again at the year end then the massive haircut that is being applied to the valuation will begin to diminish.

With renowned investors such as Bill Miller of Legg Mason and John Paulson (of subprime fame) lining up alongside Bill Ackman in holding the line firm with their positions and seeing upside of multiples of the stock price, I am happy to join them on the shareholder list.

This trade in particular is high risk but one that we believe embodies exactly the investment rule that is reward is related proportionately to risk. At $14.50 per share and trading at a small premium to book, this could be a double or trebler for 2017.

8. VIX (US Volatility measure) to rise from current level – 11

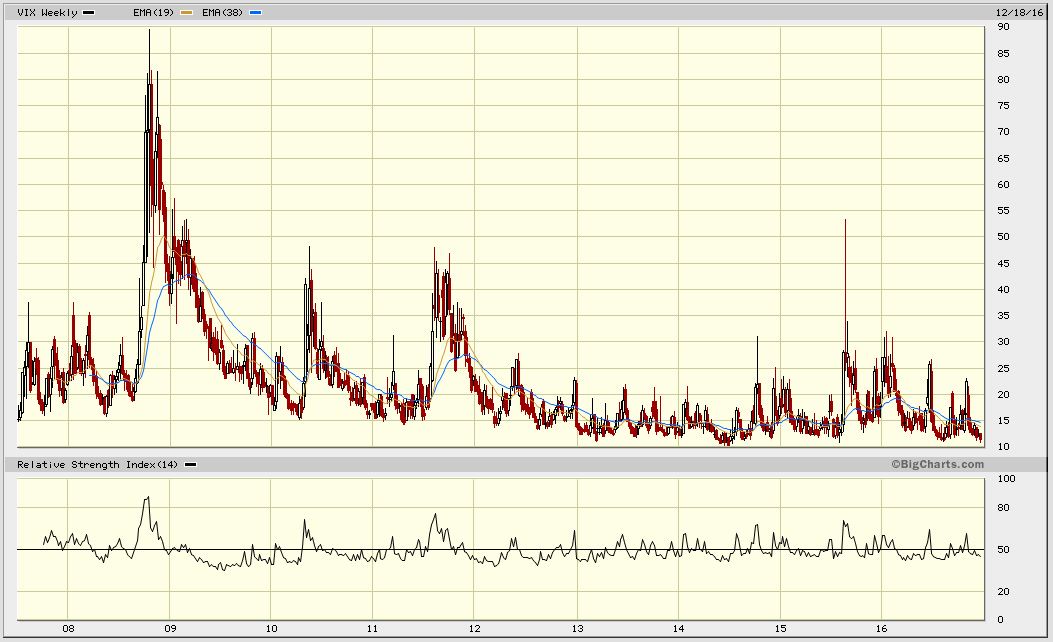

This is a slight departure from an outright stock recommendation, and one that we believe, based on historic norms and the risks to the market re “Trump surprises” and the potential for continued rises in bond yields to be a “gimme” at the current VIX level of 11.

We can see in the chart below from mid 2007 that during the long bull run that was kick started in the aftermath of the GFC that there seems to be a natural floor to the VIX measure of around 10.

Whenever it reaches this level it does not stay there for long as the market seems to find something to worry about and up goes the measure. With the potential for a trade war with China, increased terrorist activity as a consequence of Trump’s intended hard line and no mercy approach to ISIS, increasing debt burden in the States with the Trumponomics pump priming of the economy, the return of protectionism etc etc I personally feel that the risks going into 2017 are likely to rise not fall further from an already near record historic low level.

So how to play this? For those looking to be nimble and trade in and out then the ETF offering that is the UVXY which returns 2 times the exposure to the underlying VIX index. Traders do however need to be careful due to time erosion and rebalancing effects as, all things being equal, if the VIX stays the same over a period of time the UVXY actually declines. Of course, catch a timely uplift in the volatility measure and the returns can be spectacular. For those readers with a lesser risk appetite then one can gain exposure on a 1 for 1 basis to the VIX through a conventional spread betting or CFD account.

9. Gold to resume its bull trend – $1130/oz

Perhaps we are tempting fate in going for the same call as we did at the start of 2016. With the US dollar seemingly in an unstoppable uptrend and interest rates in the States likely to rise 3 – 4 times next year, many people expect the price of the yellow metal to struggle from here.

SPDR Gold chart

SPDR Gold chart

We can see in the SPDR gold chart above (a good proxy from the metal itself) that the precious metal is in fact more oversold than it was going into the start of 2016 and is approaching the multi decade low levels of early summer 2013 right before a near 20% rally ignited the price. Together with the continued reduction in CoT positioning and, as I write, an 8 week consecutive decline we are setting up for what we see as another bottoming formation and we anticipate a sharp 5-10% rally in the seasonally strong Jan – March period and expect the price to end the year towards the 2016 highs of around $1400/oz.

The best way to play such a rally, in our opinion is either a direct bet on the price of gold or, for those looking for some spice, via the GDX or GDXJ ETF’s that we highlighted in our opening 2016 piece HERE and that produced spectacular returns over the ensuing first 6 months.

10. Gulfsands Petroleum – 7.5p

![]()

A good background on the company and the opportunity is HERE and this recent piece HERE from just weeks ago also sets out the updated story post the recapturing of Aleppo by Al Assad’s Government forces. Together with the new and evolving geo-political landscape post the Trump victory, this moves the lifting of sanctions against companies operating in Syria ever closer.

As the stock has moved back to just under 8p per share, given our see through minimum price of 20p per share and possibly meaningfully higher depending upon back payments from their partner Sinochem, we continue to believe the stock a good accumulation prospect here.

Our washing is very clearly out on show here at Align Research and we continue to pioneer this unique research model in which capable, experienced and seasoned analysts really do “eat their own cooking” whilst adhering to robust PAD rules and compliance overlays (all our fully covered companies are locked in to a 6 months minimum holding period by Align). We hope that 2017 proves just as prosperous to all our readers and look forward to casting our eyes back over our calls in 12 months time.

CLEAR DISCLOSURE – The author, who is a Director of Align Research Limited, holds a personal interest in all companies mentioned in this article and is bound to Align Research’s company dealing policy ensuring open and adequate disclosure. Full details can be found on our website here (“Legals”).