It’s time to position for the second leg of the oil bull market

By Richard Jennings, CFA

Investors of some years in the markets will be familiar with the typical investor sentiment cycle that begins in despair and despondency and ends in euphoria, generally playing out over a period from 18 months to 3-4 years.

Take a look at the graphical depiction of this cycle below.

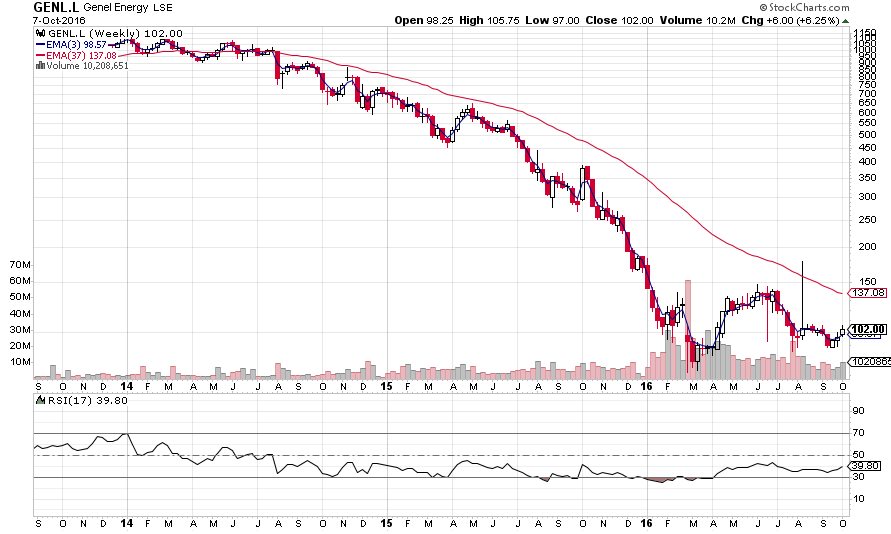

Here at Align, from being resolute bulls of commodities and thus oil at the beginning of the year (see HERE and HERE) we have watched the rally with great satisfaction and in oil’s case have highlighted the valuation opportunities in both the Gulf Keystone bonds (not the equity where these poor saps have been all but wiped out) and Genel Energy (see HERE and HERE). We also believe there to be multiples of the current stock price in value within Providence Resources as alluded to by clicking on the tab on the right in relation to our coverage of this company. The primary issue being our well voiced reservations regarding Tony O’Reilly Jnr’s ability to monetise these assets as we lay out in our open letter HERE.

Welcome news in Pat Plunkett’s appointment as Chairman at Providence Resources

In relation to PVR it was pleasing to see the appointment of ex Tullow head Pat Plunkett to the Chairman role and further his purchase of stock on Thursday in PVR, laying out £120,000 for some 1m shares – effectively the same price as the summer placing. This is a welcome example that has been set to Mr O’Reilly and his other Board members that invested woeful amounts in the $72m capital raising early summer and that left him and his acolytes open to easy criticism re mis-alignment with his (long suffering) shareholders.

Speculation is growing ever louder in City circles that the company is very close to the conclusion of the much vaunted and all important Barryroe farm out. Market intelligence also leads us to believe that the stock overhang that has bedevilled the shares for some months now has almost been chewed through (we suspect Melody was the main culprit here).

Should a farm out occur on favourable terms and a figure of $30m+ be received for half their 80% interest in Barryroe, we suspect this sum would then be used towards drilling the highly prospective Spanish Point acreage. The valuation case is binary here – a farm out will result in a further enhanced balance sheet and flexibility + good oil flows from the Druid well will drive the stock price materially higher as 2C reserves move to 2P in Barryroe’s and Spanish Points case and unrisked to 2C in Druid (and possibly Drombeg’s case).

We note that the Board struck themselves copious amounts of options with strikes at 45c. Given that ToR Jnr has all but been wiped out here (both reputationally and financially), the option vest price is a “tell” as to where they see low end valuation of PVR should the stars finally align for them. I highly doubt they arrived at an arbitrary price they believe is unachievable too…

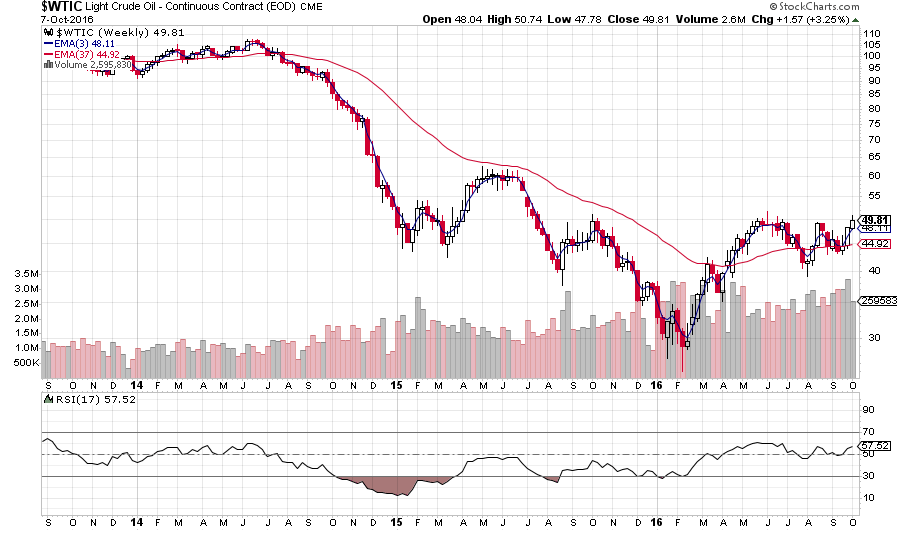

Back to the oil story – as we can see from the chart below the price of oil is now in a resolute bull trend and we are moving towards the seasonally strong winter heating season. In fact we posit that we are between the “depression” and “hope” stage of the investor sentiment cycle above.

More importantly however for the commodity going forward is the fact that many analysts see the market moving into a deficit position much sooner than expected. Quite a volte face for the many voices calling for a glut from here on out and sub $20 a barrel only 6 months ago (lesson number 1 – NEVER listen to the so called experts – “groupthink” always clouds their outlook)! During the last 5 weeks US stockpiles of the black gold have fallen by approx 5% – the fastest rate in 2 years. Global supplies are also being drained too. Couple the above with the shuttering of many oil projects by the majors over the last 2 years since OPEC shocked the world in 2014 and pursued the “beggar they neighbour” approach that collapsed the oil price from triple figures to $24 a barrel and you have, to us, the classic recipe for a sustained rise going into 2017 and beyond. Remember this market is forever a discounting mechanism (albeit moving to extremes of greed and fear) and so expectations 12 months out get priced in now.

Consensus amongst the analyst community is for a year end Brent price around $45 and that we still have a work through of supplies before a renewed platform for a price ascent north of $50 is likely. We take the opposing tack and noted the comment last week from PIRA Energy that they believe the oil market is currently now in deficit and to the tune of 500k bopd. What’s more they expect this to double by the years’ end. If this is the case we would not be surprised, indeed expect, the price to be around $60-65 a barrel.

So, to conclude, for those of you that missed the first leg of the rally, our stance is to look for the laggards that have additional potential positive catalysts to provide a double whammy if the oil price continues to rise. Top of the pack to us is Genel Energy which trades at a discount to its book value of nearly 80% and, if we adjust for the outstanding receivables due from the KRG (where the picture appears to be improving), is trading on an EV:EBITDA of probably less than 1 times. Any sniff of a large repayment of the historic receivables and these could easily double in price and still be a very cheap stock. I made the following comment in my last comment on GENL just over 2 months ago and stand ever more confidently by that statement given the shifting dynamics to the bull side in the underlying price of oil – “The call in this piece depends of course on where you see oil over the next 12-24 months. $50 b/bl and above and the stock looks a steal to me.”

Of course, for the real gamblers amongst you, the minnow that is Gulfsands Petroleum and for which we have covered in depth HERE, could provide serious multi-bag returns should Block (26) be sold/sanctions removed in Syria.

CLEAR DISCLOSURE – The author, who is a Director of Align Research Ltd, holds a personal interest in Genel Energy, Gulf Keystone Convertible Bonds and Gulfsands Petroleum & is bound to Align Research’s company dealing policy ensuring open and adequate disclosure. Full details can be found on our website here (“Legals”).