Our three blue-chip commodity Conviction Buys for 2016

By Richard Dennis, CFA

Over the last few months we have continued to see the commodity sector struggle. Much of the attention has focussed on the oil price drop and the woes of many natural resource companies given the ongoing headwinds in the asset class. There has also been much discussion over when, or indeed if, commodity prices will recover, and even whether some blue-chip companies can survive for much longer.

With this is mind it is worth pointing out it was only a few years ago there was as much discussion about commodity prices staying high forever, along with the probability of the entire natural resource sector getting a permanent improved re-rating in the equity markets. We didn’t believe in the higher forever scenario, just as we don’t believe in the current consensus bearish view.

Over the medium-term it appears that the upside is still capped for oil and most industrial metals, but it is important to remember how important the direction of the US dollar is to the commodity sector, and in reality to all asset classes.

There was much fanfare surrounding the first rate rise by the Fed just before Christmas, but strictly speaking monetary policy started to tighten in the US over two years ago when bond purchases were reduced. The rise in the US dollar and difficulties for emerging markets and commodities over that time frame is consistent with this. In previous cycles Western central banks have followed suit not long after the Federal Reserve, yet this time there does not appear to be that commitment.

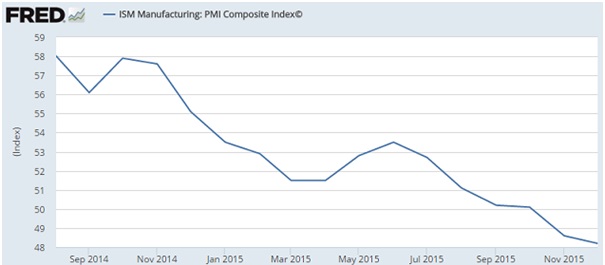

As such, continued US dollar strength is very possible during 2016 given such loose monetary policy elsewhere in the world. In turn this could cause problems back in the US given it could worsen a slowdown if economic growth disappoints. The ISM manufacturing index is already below 50 (indicating manufacturing contraction) and GDP growth, while still healthy, has also been declining for more than a year.

With the current economic growth cycle already stretched in terms of longevity, the possibility of another downturn when rates are already only just above zero raises the spectre of an even more powerful version of quantitative easing. This would change the outlook for gold and precious metals significantly for the better.

With GDP growth in the US falling we expect more market participants to gradually consider the implications of another down cycle, and to buy precious metals in anticipation of a more dovish Fed and a potentially weaker US dollar.

One of the first sectors to benefit from this eventuality would be the blue-chip gold and silver mining companies. As businesses that are inherently highly leveraged to the underlying commodity price it is not a surprise that the precious metals sector has been severely sold down since 2012, particularly so in recent months as operating margins have been severely squeezed. Many companies have raised capital during the last decade, only to find that new operations have failed to live up to expectations, and have been punished in the market accordingly.

One of exceptions to this is Randgold Resources (RRS), which despite facing the same headwind of falling precious metals prices, has been managed on the basis that the gold price will have sustained periods of weakness, such as the one currently being experienced. As such, the company is well positioned to deal with the bullion price today and very well-positioned to benefit from what we believe will be a rising gold price over the next few years.

Randgold’s three main mines – Loulo in Mali, Kibali in the DRC, and Tongon in the Ivory Coast, are all large established low cash-cost and long mine-life operations, and the company produces in total approximately 1.1 million ounces (moz) of gold per annum at a cost of around $700/oz. While other companies have seen production levels fall and cash costs rise due to lower mined grades, Randgold has quality assets and has managed to keep both grade and production relatively steady in recent years. With no debt and a healthy cash balance of $168 million it can continue to fund exploration to bolster what is already an impressive reserve and resource base of 15moz and 21moz respectively. The company hit new record production levels during Q3 2015 and despite seeing profits decline to $48.8 million from $59.2 million, primarily due to the 6% quarter-on-quarter decline in the gold price, is doing well.

Typically, when investors start to believe that there is a period of improving gold prices ahead, they generally head for companies that can benefit immediately from this change. Randgold is one of the few global gold producers who fit the bill, and are considered by us a Conviction Buy.

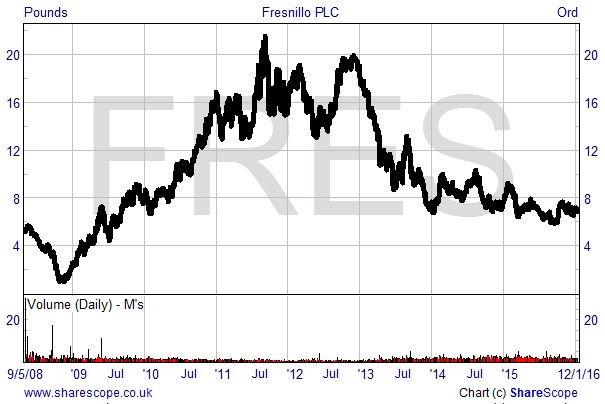

Rising precious metal prices would also benefit Mexico and London listed Fresnillo (FRES). A much older and slightly different company to Randgold, it produces an equally impressive 45moz of silver and almost 600,000 oz of gold per annum. Its reserve base exceeds 500moz silver and 2moz gold. Despite experiencing operational problems recently at its flagship Fresnillo mine, Saucito and Herradura, it is hopeful of achieving production levels of 65moz silver and 750,000 oz gold by 2018.

If the company can manage to get even close to these levels in two years time then given our optimistic outlook for gold and silver prices, investors should be well rewarded. In the very short-term investors may need to be nimble given the current operating difficulties, and owning the stock during the earnings season carries similar downside risk to other commodity producers at the moment. However, Fresnillo’s impressive reserve base and production outlook makes the shares another Conviction Buy.

Cash in copper?

Although the outlook for the rest of the commodity sector is not as compelling as it is for precious metals at this juncture, we need to highlight again how much of the current weakness in the sector relates to US dollar strength.

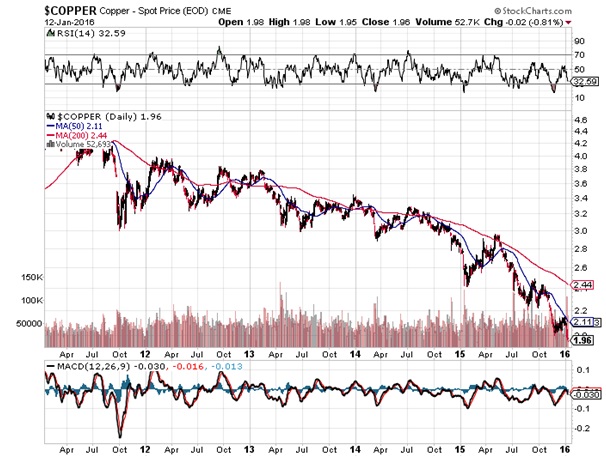

While it is possible that the current trend continues in the short-term, we have already seen a widespread liquidation of commodity exchange-traded funds in the last two years which has exacerbated the problem of falling prices. The recent collapse in the copper price would at first glance indicate that demand has gone the same way and that the copper market is in severe oversupply.

But in reality, demand in China improved towards the end of last year, with sharply rising imports, and inventories down to less than two weeks supply. Mining company order books are also improving. While none of these details are likely to protect the copper price if the US dollar continues to appreciate, they do suggest that the copper price could rebound sharply in the weeks ahead, and not just because of currency moves.

This brings us to London-listed copper producer – Antofagasta (ANTO). Its share price has collapsed by almost 50% in the last six months as the copper price plummeted. Many other global copper equities have suffered to an even greater extent. Despite this the company still looks well-placed to benefit from a change in sentiment, which we believe will occur this year.

While a number of copper mines in Africa have been closed due to cost, Antofagasta’s mines in Chile are very low-cost at little more than $1.15/lb. Although operationally it has had some minor problems recently, and much of the expansion plans may not necessarily lead to a big increase in overall group production, we believe the recent acquisition of the Zaldivar copper mine may prove to be timely. The Antucoya project should resolve its commissioning issues and achieve the target 85kt copper per annum.

Given what we are seeing across all mining stocks at present, timing an entry into this stock is not easy, but looking through current volatility there is a strong case to be made for another low-cost producer such as Antofagasta. It is also a Conviction Buy.