Leni Gas Cuba – Further progress at the operational and corporate levels. See through price 2.74p – 4.67p

By Richard Gill, CFA

Since we initiated coverage of Leni Gas Cuba (LGC) on 8th April the company has seen a number of positive developments across its portfolio of investee companies and at the corporate level. In addition, the Cuban government has demonstrated further liberalisation of its borders and another London listed company, Rose Petroleum, has made moves to invest in the Cuban economy.

TRAVEL – strong trading from inCloud9/Travelwelcome

As alluded to in a February update, LGC’s 40% owned Cuban travel and concierge business inCloud9/Travelwelcome Group had a strong quarter of trading in the three months to March. Unaudited consolidated revenues for the period were up by 108% compared to the previous quarter, at US$407,000. This came on the back of a significant increase in the number of bespoke itinerary visitors attracted by events such as the Havana Cigar Festival. The numbers being delivered so far seem to support the company’s claims that inCloud9/Travelwelcome Group has the potential to be a multi-million dollar revenue business.

We see further good opportunities for this business as the Cuban tourism industry continues to grow. According to Tourism Minister Manuel Marrero, Cuba saw 1.5 million tourists in the first four months of 2016, up by 13.5% compared to the same period in 2015. Notably, there was a 93% rise in visitors from the US, with 94,000 travellers coming to the country on the back a relaxation of travel restrictions.

While US citizens are still banned from travelling for “tourism” the restrictions have been relaxed to such an extent that the first US cruise ship to arrive in Havana for 50 years (the Adonia) docked with 700 passengers on 2nd May. This came after the Cuban authorities lifted a ban on Cuban born residents only being able to re-enter or leave the country by air – from 26th April the entry and exit of Cuban citizens, regardless of their immigration status, as passengers and crew on cruise ships is permitted. Operator Carnival, trading under the Fathom Travel brand, is now offering week long cruises on the Adonia, with associated “cultural activities” on the island, which will depart from Miami on a fortnightly basis.

OIL – MEO Australia shares advance on Cuba attractions

Leni Gas Cuba has a 15.8% interest in ASX listed oil exploration company MEO Australia which owns a 100% interest in the 2,380km2 onshore oil block, Block 9 PSC in Cuba. MEO is currently completing a preliminary assessment of Block 9 and reprocessing 2D seismic data.

At the end of April MEO released its quarterly report for the three months to March. Although there was nothing really new in the release, MEO did confirm that the prospectivity assessment is expected to be concluded in mid-2016, as previously flagged. MEO’s cash balance stood at AUD$4.95 million at the period end, with the estimated outflow for the current quarter being AUD$1 million.

We note that since LGC’s initial subscription on 29th February at a price of 1c per share, MEO Australia shares have risen to a current mid-price of 1.85 cents (as at 18th May) valuing LGC’s stake at AUD$£1.6 million (£1.32 million) – representing c.20% of the current market cap alone.

MEO Australia share price. Source: ASX

Sporting venture with Rushmans opens up access to a new sector

Prior to listing on ISDX in November last year, LGC entered into a strategic alliance with consultants Rushmans in order to identify Cuban investment opportunities. The first deal has now been formalised, with the two parties having formed a 50/50 joint-venture to explore the opportunities for international entities to participate in development funding for Cuban sport.

Under the deal, Rushmans will grant the joint-venture an exclusive licence to use the Rushmans brand and intellectual property in respect to Cuban sporting opportunities. In return, LGC will pay £100,000 to fund the accepted projects and also provide an initial £40,000 for working capital. The working capital funds will be repaid before any pro-rata distributions.

Rushmans looks to be an excellent partner, having 25 years’ experience providing sports consultancy services. It has advised and supported sports governing bodies and played a role in planning and delivering a host of major events including the football European Championships and cricket and rugby World Cups. Reflecting the value that the consulting firm could bring to the business Rushmans was issued options over 50 million shares in LGC on admission to ISDX, with exercise prices ranging from 2p to 20p per share, all at a premium to the current market price and illustrating both parties’ expectations of the value of CUBA.

This deal ties in with a Cuban sporting industry which looks ripe for investment and growth given that the US embargo has made it difficult for the sector to make the investments required for the country to compete at the very top level with other sporting nations.

Entry into renewable energy via solar deal

Leni Gas Cuba has also entered into another new sector via a joint venture with UK solar power and storage specialists, Commercial Funded Solar Ltd. The deal is to assess the potential for installing and operating renewable energy and hybrid power solutions (solar power, energy storage and integrated power management systems) in Cuba. This targets a market in which the Cuban government is aiming to produce 24% of its electricity from renewable sources by 2030.

Both parties will lead the development and construction of each project, with funding coming from external investors. They will share on a 50/50 basis the development, funding and construction revenues for each renewable power plant built, and share on a 75/25 basis (75% to CFS) the 10-20 year operational contracts for all systems.

Possible reverse takeover opens up Canadian listing – see through price of 2.74p to 4.67p per share

Perhaps the most significant news of the past few weeks is that LGC has signed a letter of intent with TSX Venture Exchange listed investment shell Knowlton Capital (KWC) in relation to a potential all share reverse takeover.

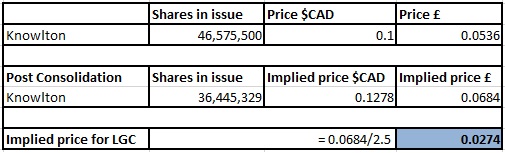

The mechanics of the proposed deal will see Knowlton issue 197.6 million shares for LGC following a 0.7825 for 1 consolidation of Knowlton’s current 46,575,500 shares. LGC shareholders will receive 1 Knowlton share for every 2.5 LCG shares they hold and following completion will own 84.43% of the enlarged company.

Trading in Knowlton Capital shares has been halted from trading since May 2014 after the company announced the proposed reverse takeover of Mongolian mining business Mogul Ventures. This transaction has now been cancelled following the LGC agreement. Completion of the reverse takeover is subject to, amongst other things, completion of due diligence by Knowlton, receipt of regulatory approvals and approval by LGC shareholders.

Of course there is uncertainty at present as to what the exact post consolidation price will be until Knowlton shares resume trading. While the last traded Knowlton share price of CAN$0.1 is almost two years old it implies (at the current GBP/CAN exchange rate of 1:1.853, post consolidation and assuming the Knowlton price holds steady) an equivalent takeover price of 2.74p per share for LGC, or £13.5 million. This compares to LGC’s current mid-price on ISDX of 1.3p and a market cap of £6.4 million.

Leni Gas Cuba “see through” price based on last traded Knowlton price of 10c. Assuming GBP/CAN rate of £1:$1.853

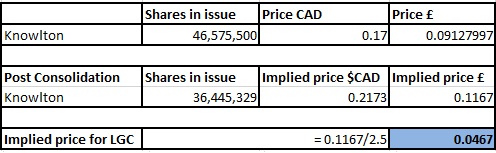

While trading in Knowlton shares is halted on the TSX Venture Exchange, bid and offer prices are currently live.(Source http://web.tmxmoney.com/quote.php?qm_symbol=KWC.H). Current indications are that the post deal price will be at a material premium to the last pre-halt price of 10 cents, with current queued bids standing at 17 cents. This equates to a “see through” price of 4.67p, again assuming that the Knowlton price holds post consolidation.

Leni Gas Cuba “see through” price based on last quoted Knowlton bid price of 17c. Assuming GBP/CAN rate of £1:$1.853

This potential deal shows that Leni Gas Cuba is making further progress on its stated goals mentioned in the ISDX admission document, with a North American listing being one of the key objectives. Canada has good relations with Cuba, having maintained positive relations with the country despite the sanctions imposed by its neighbour, the US. A number of Canadian companies have subsidiaries operating in Cuba and the island is a popular travel destination for Canadian citizens – according to the Canadian government over 1 million Canadians visited Cuba in 2014, making up 40% of all international visitors.

While the Knowlton deal will add minimal balance sheet value to the enlarged group, it will, if completed, open up access to the Canadian capital markets and bring with it an experienced team of directors, including Jeremy Edelman and Mazen Haddad, who are well known to the LGC executive team. LGC has also stated that it would look to maintain its current ISDX listing “if deemed appropriate”.

AIM listed ROSE scents Cuba opportunities

In developments elsewhere, we note that Cuba has attracted investment interest from another London listed company. On 3rd May AIM listed Rose Petroleum (ROSE), which is diversifying away from its core oil & gas portfolio, raised £800,000 specifically to invest in opportunities around the processing and manufacturing of gypsum and associated building materials. The company sees “significant near term opportunities in the Cuban construction industry” and is currently in discussions with a Cuban Government owned company, which has extensive gypsum resources and reserves for exploitation, together with the relevant Ministries in Havana, over a potential transaction.

ASSESSMENT

One month on from our initiation of coverage on Leni Gas Cuba the company has demonstrated further progress towards its stated aims. Of course, significant risks remain to the investment case including the sole focus on Cuba, Cuban political risk, successfully implementing the investment policy, exposure to US government policy, the oil industry and exchange rate risks.

Given the early stage nature of the business, and the speed at which deals are being done, we are not introducing forecasts at this stage but will do so in due course when the various strands of LGC’s business interests achieve a base from which projections can be made. However, we continue to see significant potential upside from current levels given the opportunities discussed, with the 2.74p – 4.67p implied reverse takeover price acting as a potential short-term indicator of value.

CLEAR DISCLOSURE – Leni Gas Cuba is a research client of Align Research. Align Research owns shares in Leni Gas Cuba. A Director of Align Research holds a personal interest in Leni Gas Cuba and is bound to Align Research’s company dealing policy ensuring open and adequate disclosure. Full details of our Company & Personal Account Dealing Policy can be found on our website http://www.alignresearch.co.uk/legal/