Kazera Global – Positive read over from Namibian peer Arcadia Minerals. Buy.

By Dr. Michael Green

Namibia seems to be fast shaping up to become a hotbed of tantalum and lithium – critical metals which are essential for the modern era and the transformation to a low carbon world.

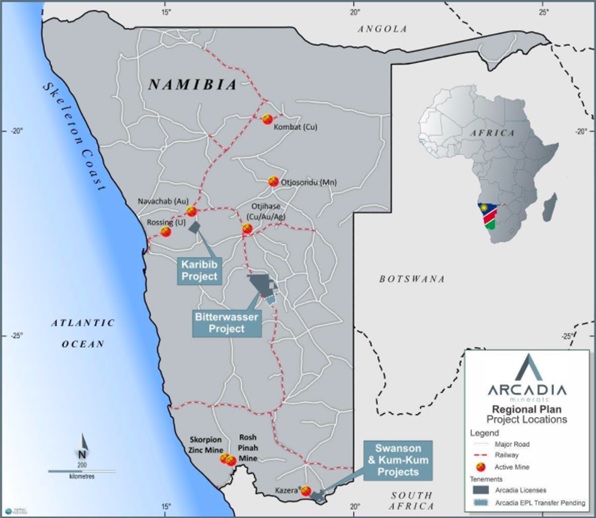

A really interesting Namibian play started trading in Australian in June this year. Arcadia Minerals (ASX:AM7) is a diversified explorer seeking mainly battery metals focused on this country. Arcadia’s flagship asset looks to be its advanced Swanson Tantalum project, plus there is the battery metals portfolio which is made up of the Kum-Kum Nickel Project, the Bitterwasser Lithium in Brines and Lithium in Clays Project and the Karibib Copper Project.

Location of Arcadia Resources projects in Namibia. Source: Arcadia Resources website

Arcadis’s Swanson Tantalite Project lies adjacent to Kazera’s Tantalite and Lithium Project in the south of the country just north of the Orange River that forms the border with South Africa. Arcadia’s Namibian subsidiary Orange River Pegmatite (Pty) Ltd (ORP) owns a 14,672km² Exploration Prospecting Licence (EPL) 5047 that contains the Swanson Tantalite project which lies 15km north of the Orange River.

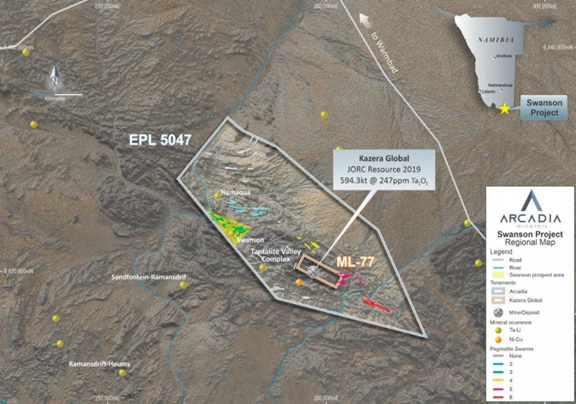

According to Arcadia’s website, EPL 5047 covers a mountainous desert setting characterised by a complex geological and structural setting with good mineralisation potential amplified in the presence of large shear zones (Tantalite Valley Shear Zone) and a neighbouring intrusive mafic-ultramafic body, with appreciable Cu and Ni mineralisation.

On Arcadia’s property, a large number of well-mineralized pegmatites are also present. These occurrences are demonstrated by the presence of extensive, small-scale mining activities where tantalum, beryl and spodumene have been extracted in the past from these pegmatites. The extent of this mineralisation is indicated by the name Tantalite Valley. Kazera’s active tantalite mining operation is at Mining Licence 77, see the map below.

Arcadia’s Swanson Project regional map. Source Arcadia Resources website

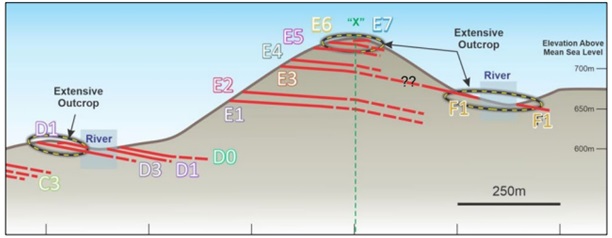

Well-respected mining consultants Snowden produced a report on the geology and mineral resources of the D and F pegmatites for ORP/Arcadia at the Swanson Tantalite Project. This maiden MRE quantified the outcropping and shallow resources on four (D0, D1, D2 and F) of the 15 pegmatites.

Swanson Tantalite Project – section through the D, E and F pegmatites. Source: Snowden Sept 2021

Apparently, these pegmatites are a pretty uniform thickness of around 1.5m to 2.5m, are tabular, non-zoned, gently dipping and contain tantalum, niobium and lithium mineralisation. Geological continuity of the pegmatites was established through mapping and taking chip and channel samples of surface exposures, with the extension of these pegmatites under shallow cover determined by diamond drilling.

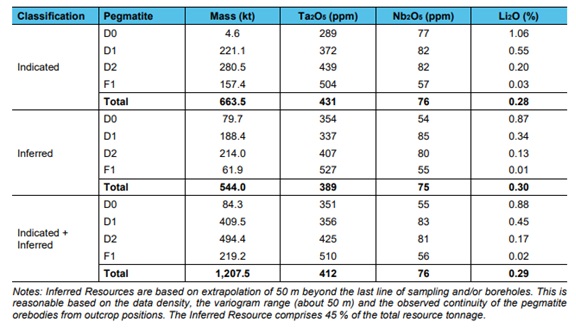

Maiden MRE for Arcadia’s Swanson Tantalite Project – ORP D and F pegmatite Indicated and Inferred Resources as at 1 September, above 236ppm Ta2O5 cut-off.

Source: Snowden report for ORP September 2021

As can be seen in the MRE table above, around 76% of the reported tonnage is contained in the D pegmatites. Meanwhile, the Ta2O5 average grades at the F pegmatite are 23% higher at 504ppm Ta2O5 compared with 408ppm Ta2O5. Lithium grades are seen to be lower at the F pegmatite than in the D pegmatites, with the highest lithium grades found in the D0 Pegmatite, at 1.06 % Li2O. The geological and grade continuity of the pegmatites was sufficient to classify the reasonably well explored area as Indicated Resources, with Inferred Resources being extrapolated fifty metres beyond the last line of sampling.

Consultant Snowden’s report highlighted the prospects for eventual economic extraction at the Swanson Tantalite Project. The suggested mining operation was an open pit mine with a maximum stripping ratio of 4:1 stripping ratio before going underground. Processing and metallurgical assumptions were based on a 5.45t bulk sample which demonstrated that the ore was easily crushed, with spiral recoveries on the rougher spirals expected to be in the 70-80% range.

On the mineral processing, it was pointed out that with a 76% spiral recovery and a 90% MGS recovery, it was thought possible to be able to produce a Ta2O5 concentrate at over 20% Ta2O5 with a recovery of around 68%. Apparently, a financial model was produced using ORP/Creo Design resource number and mining design parameters, showing that the project produces a positive NPV, but this report didn’t give away any NPV results or the IRR.

At the time this report was published further drilling (1,100m) was underway at Swanson which Snowden believed would help improve the geological modelling and the grade estimation. The consultants believed that the issues which needed to be addressed during the next estimation exercise included: density modelling, better definition of the nugget effect from downhole samples, definition of any anisotropy (the predictable variation of a property of a material with the direction in which it is measured), definition of the lateral extent of the F pegmatite, and whether the F pegmatite joins up with one of the E pegmatites, modelling and resource estimation of the E pegmatites and an investigation into the extensions to the D and F pegmatites.

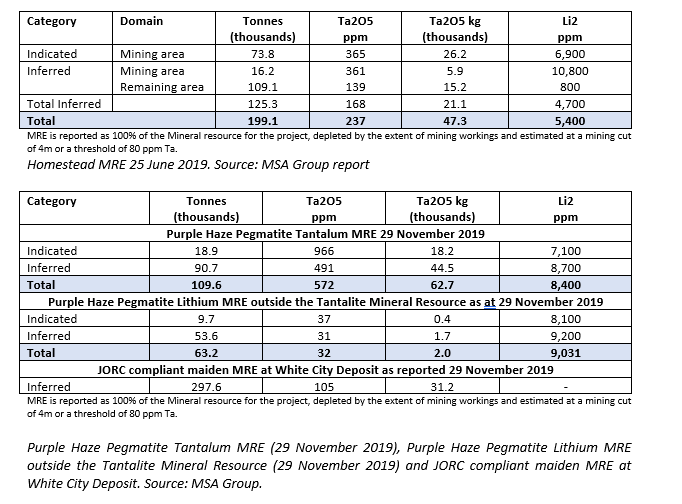

In a nutshell, Arcadia is an exploration company which has just determined a maiden MRE at its Swanson Tantalite Project where consultants think that are reasonable prospects for eventual economic extraction. Arcadia currently trades at A$0.20 a share, with a market cap of £9.36 million and an Enterprise Value of £5.95 million. Contrast this with Kazera that has the all important Jorc resource estimate of @ 669.6k tonnes of lithium & tantalum and thus should warrant a higher valuation than pre Jorc at inferred status as in Arcadia’s case.

So, what might Kazera’s Tantalite and Lithium Mining Project next door really be worth with a Mining Licence in place, mine in place, processing plant in place and substantial capex already invested? The first commercial delivery of tantalum is on the cards to be exported before the end of the year, with well-developed plans to steadily increase volumes to more than 10,000 kilograms per month by the end of 2022. One thing for sure is that little of the realistic valuation for such a mine is currently being reflected in Kazera’s lowly market cap of £9.8 million at the current 1.30p per share. Alongside all this progress, the team will also be focusing on establishing further mineral reserves as well as on developing the company’s lithium opportunities.

That is not to mention the swiftly changing fortunes at all other Kazera’s projects. New financing arrangements have just been put in place will allow all the company’s existing operations to be trading profitably before the end of the year (2021). Here we are talking about the alluvial diamonds mining operation and the diamond processing operation which the company has recently taken control of at Alexkor.

At the same time, within 6 months of the Mining Permit for the Heavy Mineral Sands (HMS) operation being granted the board expects to substantially boost positive cash flow generation, with the company talking about starting to generate some US$300,000 per month of cash. It has to pointed out that these sorts of numbers are planned to be further improved by bringing in a third party to build and operate a separation plant on the HMS side. Whilst all this is happening, the company looks to be making progress on an application for a Prospecting Right over an area which is something like 34 times bigger than the current site.

Now here’s the neat & unique thing from a mining perspective. As HMS is being mined, diamond production will also increase as they are both in the alluvial sands. On this subject the board is talking about an estimated increase in diamond production of an additional 300 carats per month and these are better quality stones which are confidently anticipated to be sold at auction at an enhanced price of US$750 per carat. Readers can see why it is easy to run out of superlatives when writing about Kazera.

We continue to believe & illustrate that the company is well undervalued by any yardstick. The peer comparison with Arcadia as we have laid out here for an adjacent earlier stage project demonstrates this only too well. We initiated coverage on Kazera with a Conviction Buy stance in August 2020 at 0.70p with a target price of 2.50p. In the last 14 months so much progress has been made on many fronts. This will be well and truly shown when we publish an updated research report with a highly revised target price. With the shares currently trading at a derisory 1.3p, we are more than happy to reconfirm our Conviction Buy stance ahead of a hoped for long-awaited proper re-rating of this out and out growth stock.

RISK WARNING & DISCLAIMER

Kazera Global is a research client of Align Research. Align Research is the largest shareholder in Kazera Global and as such cannot be seen to be impartial in relation to the outcome of the Company’s share price. Align Research & its Director are bound to the company’s dealing policy ensuring open and adequate disclosure. Full details can be found on our website here (“Legals”).

This is a marketing communication and cannot be considered independent research. Nothing in this report should be construed as advice, an offer, or the solicitation of an offer to buy or sell securities by us. As we have no knowledge of your individual situation and circumstances the investment(s) covered may not be suitable for you. You should not make any investment decision without consulting a fully qualified financial advisor.

Your capital is at risk by investing in securities and the income from them may fluctuate. Past performance is not necessarily a guide to future performance and forecasts are not a reliable indicator of future results. The marketability of some of the companies we cover is limited and you may have difficulty buying or selling in volume. Additionally, given the smaller capitalisation bias of our coverage, the companies we cover should be considered as high risk.

This financial promotion has been approved by Align Research Limited