Pricing Providence Resources going into the drill of 2017

By Richard Jennings

As the drill bit prepares to be turned on the South Porcupine basin offshore the South West coast of Ireland (licence known as FEL 2/14) we take a look at some potential share price implications (and suspend reservations that are well known on our part ref ToR Junior).

The licence areas know as Druid, Drombeg & Diablo are estimated to hold just under 6.5bn barrels of oil – a monster drill by anybody’s measure and, it is safe to say, not just company changing but country changing for Ireland should there be success with the drill bit. Providence’s current net WI in these licences equates to 3.225bn barrels of oil. This would be reduced by 35% however should Total, with whom the parties to the FEL 2/14 licence area entered into an option agreement, actually farm in. In this case PVR’s resultant interest would then be a little over 2bn barrels of oil.

Licence area

The balance sheet of PVR looks to sit with just under 50m euros of cash at this point after the sunk cost receipt of $2.265m from Cairn and the inclusion of the Total first part of the option payment of a net $16.2m to Providence. Should Total farm into the 35% interest then PVR receive an additional $5.4m and, make no mistake, if there is a strike of the black stuff Total will farm in.

The beauty of the current drill deal is that two prospects are now being drilled at both Druid and Drombeg. Net cost to PVR has been brought down to just under $18.5m or $13.1m should Total exercise their option. I must admit that this is an exceptional position for PVR shareholders to be in with regards to potentially validating 2bn barrels of oil for relative buttons on a global E&P cost basis.

Let us look at the two extremes re this drill then and assume in the first instance a complete failure with the drill at both Druid and Drombeg. In this scenario the company would sit with around 30-35m euros (allowing for some corporate overhead this last 6 months since the cash position was announced of 31.4m euros at end Dec 16). With just under 600m shares this would, at current FX rates, equate to around 5p per share of cash. While “all lines appear dead” on Spanish Point and, as we touch on below, Barryroe just cannot be brought over the line, we note that the market is now pricing effectively zero in the way of value to shareholders in this circa 472m boe net to PVR from these two prospects. Any news here re drilling/farm-in that validates the 2P status will add potentially a material amount to the market cap and enhance the attractiveness of the company to a wholesale acquirer. We estimate based on peers in the North Sea region that the value to PVR on the validation of these reserves could be worth around 80c – $1.40 per boe.

In effect we are saying that the “option value” ref Barryroe and Spanish point would, even at the lower end of 80c per boe, more than underpin the current 18.5p stock price as this would be equivalent to 49p per share should the market value these on a catalyst at this lowly figure (using current FX rates of USD:GBP $1.29). At a $1.40 per boe then the upside is a further 36p per share. Of course these are pre farm in figures but still, assuming even a nil back cost recovery and reducing the company’s interest down to a combined 30% WI with a farminee, it is very clear there is no discernible value in the stock price for these prospects at this point. This provides for potential “surprise” upside.

Now let’s look at a scenario where there is success on the drill.

Valuing the twoprospects at 80c net to PVR (assuming that Total farm in on their option exercise) results in a shade over £2 per share of 2P reserves being added. This figure alone illustrates the sheer magnitude of this drill on a global scale. Throw in the implications for Diablo and Newgrange and it is apparent what the value implications are for PVR shareholders during this important month of July 17.

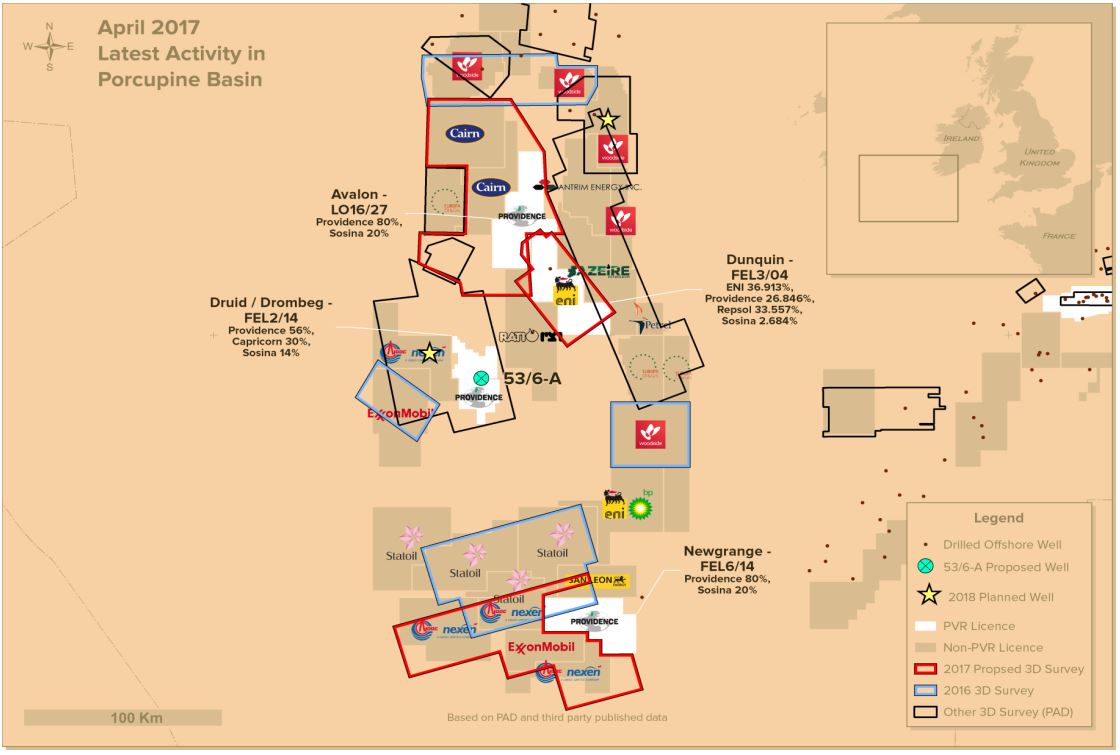

The diagram below is telling to us too with regards to the calibre of PVR’s neighbours in the Southern Porcupine region. Validation at Drombeg and Druid of the estimated reserves will not go unnoticed and again adds weight to the PVR takeover thesis that has done the rounds in recent months in the City.

Southern Porcupine neighbourhood

So we have a band of 5p per share net cash and zero value for the entire remaining licences spectrum against upwards of ten times the current stock price in the event of success at Druid and Drombeg. Within this band you can place a CoS on the well drills and that has been estimates at anywhere between 10% and 30%. Applying the 10% CoS would imply an optionality in the stock price of 20p + 5p net post drill cash and still be ascribing zero value to the rest of the company. One can take their own figure on the CoS and apply against the £2 net 2P increment at an 80c boe valuation and come up with a variety of figures. However, whichever way we splice it, is seems clear to us that the “O’Reilly” discount is still embedded in the stock price. For those of a risk orientated nature this provides opportunity.

In conclusion, at the current price we see the risk/reward continuing to be materially asymmetrically skewed to the upside, most likely as a consequence of the failure of ToR Jnr to finally conclude the Barryroe deal and of which I have given him much criticism. Thankfully, the importance of this field for the company going forward is diminishing and with the clear interest by the oil majors in the Atlantic Margin we suspect that a successful drill as we move through July will, aside from adding a material amount of new 2P reserves, probably catalyse a complete acquisition of the company. To this end we also note the option strikes for the directors at 45c euro cents and that expire in August 2019. This should give some indication of where management see, on a successful validation of the Atlantic Margin prospects, a takeout being materially north of this figure as we have highlighted above.

Accordingly, we stand pat (excuse the pun) with Providence Resources being one of our top 10 Conviction Buy picks and eagerly await, along with other PVR shareholders, the results of the “drill of 2017”.

DISCLAIMER & RISK WARNING

The author, who is a Director of Align Research Ltd, holds a personal position in the equity of Providence Resources and is bound to Align Research’s company dealing policy ensuring open and adequate disclosure. Full details can be found on our website here (“Legals”).

This is a marketing communication and cannot be considered independent research. Nothing in this report should be construed as advice, an offer, or the solicitation of an offer to buy or sell securities by us. As we have no knowledge of your individual situation and circumstances the investment(s) covered may not be suitable for you. You should not make any investment decision without consulting a fully qualified financial advisor.

Your capital is at risk by investing in securities and the income from them may fluctuate. Past performance is not necessarily a guide to future performance and forecasts are not a reliable indicator of future results. The marketability of some of the companies we cover is limited and you may have difficulty buying or selling in volume. Additionally, given the smaller capitalisation bias of our coverage, the companies we cover should be considered as high risk.

This financial promotion has been approved by Align Research Limited.